Tax planning is one of the very important aspects of financial management. A person can significantly impact their overall tax liability by understanding various deductions. Among these, Section 80C of the Income Tax Act, of 1961, is a prime area for tax savings. Section 80C of the Income Tax Act is a great way in India to get tax benefits for people. This section lets the individual claim a deduction on specific investments and expenses, thereby reducing taxable income. Section 80C lets the taxpayer save while contributing to the economic growth of the nation.

What is Section 80C?

Section 80C is a part of the Income Tax Act 1961, and it gives tax benefits to Individuals and Hindu Undivided Families. The taxpayers have to make investments and expenditures for tax savings. An individual taxpayer and Hindu Undivided Families can save tax up to Rs. 1.5 lakh per year. These tax-saving schemes are not applicable to corporate bodies, partnership firms, or other business entities.

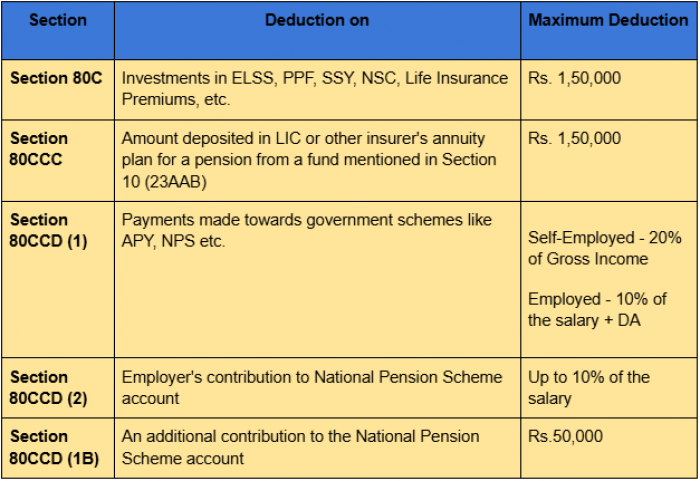

Restrictive Benefits On Sections 80C, 80CCC, 80CCD(1) and 80CCD (2)

Deduction on Income Tax of Person is as follows:

Benefits to be looked into under Section 80C

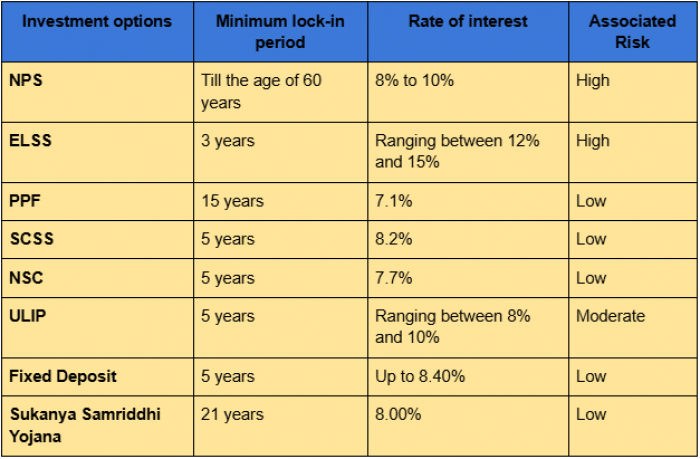

The lists of eligible investments for Tax Saving is as follow :

Benefits for the Investments under section 80C

Eemployee Provident Fund (EPF)

Epf, employee Provident Fund contributions come in section 80C benefits under Income tax Act.

Public Provident Fund (PPF)

Public Provident Fund (PPF) is a popular long-term saving scheme and investments made into PPF accounts are eligible for deductions under the Income Tax Act. The interest earned and maturity amount are tax-free.

Life Insurance Premiums

Premiums paid on life insurance policies for the taxpayer, his spouse, or children are covered under the income tax deduction. However, the policy should be either in the name of the taxpayer, his spouse, or his child.

Sukanya Samriddhi Scheme

An individual can open a Sukanya Samriddhi account for his girl child from her birth until she turns ten years. The interest so accrued comes under the income tax saving scheme.

Equity-Linked Saving Schemes

ELSS is a type of investment in a mutual fund that enables the dual benefits of capital appreciation along with income tax savings. Investments done in ELSS are eligible for relief under Section 80C of the Income Tax Act.

National Savings Certificate (NSC)

A five-year lock-in period NSC is a type of fixed-income investment. Investments under NSC qualify for Section 80C deductions in the Income Tax Act.

Tax Saving Fixed Deposit

Some fixed deposits with banks and financial institutions also come in the tax-saving category of Section 80C in the Income Tax Act. These deposits have a lock-in period of five years.

Tuition Fees

Any payment towards tuition fees of children for their education in school, college, university, or any other educational institution, are eligible for tax deduction under Section 80C of the Income Tax Act.

Repayment of home loan principal amount is tax-deductible under Section 80C of the Income Tax Act.

Stamp duty and registration charges are tax-deductible.

Stamp Duty and Registration Charges paid at the time of buying a property are eligible under Section 80C of the Income Tax Act.

NABARD Rural Bonds

The National Bank for Agriculture and Rural Development offers Rural Bonds. These bonds are deposited to claim tax benefits under Section 80C of the Income Tax Act.

Infrastructure Bonds

People, who invest in these bonds, can deposit them for income tax deductions up to Rs.1.5 lakh under Section 80C of the Income Tax Act. These bonds are issued by infrastructure companies to people.

Senior Citizen Saving Scheme

Only those above 60 years of age can invest in these schemes. They are low-risk and can help avail up to Rs.1.5 lakh tax benefits under Section 80C of the Income Tax Act.

Unit-linked Insurance Plus (ULIPs)

ULIPs provide tax benefits amounting to Rs. 1.5 lakh in a single year under Section 80C of the Income Tax Act. ULIPs also provide handsome returns over long periods.

Section 80C of the Income Tax Act 1961 serves as an excellent source for the savings options of any person earning taxable income. A taxpayer can, with proper planning of investments and expenses, reduce his tax liability and save for his future. Assessment of individual financial goals and appropriate choice of investment for the maximum benefits under Section 80C is very important.

The financial scenario changes with every passing year, and each taxpayer should be abreast of the provisions of the Income Tax Act.

Tax laws are amended and, therefore, it would always be better to keep one updated with all the amendments.

Frequently Asked Questions

Q.1 What is Section 80C of the Income Tax Act?

This investment under Section 80C in the Income Tax Act of India is one that is permissible for individuals and Hindu Undivided Families to claim relief on particular investments and expenditure. This section allows up to a maximum of Rs. 1.5 lakh of deduction.

Q.2 What is the type of investments and expenses allowed under Section 80C?

It includes such things as are adding to EPF, Public Provident Fund, paying life insurance premiums, adding to ELSS, contribution to SCSS, issuance of National Saving Certificate (NSC), tax-saving deposits, charges and duty connected with stamping a register, the fees relating to children education, repaying the capital of an accumulated home loan.

Q3. Is the amount for exemption under section 80c is confined only?

The maximum amount that can be availed under Section 80C of the Income Tax Act is Rs. 1.5 lakh. This limit will not be exceeded at all in order to achieve tax savings

Q.4 Are NRIs able to save tax under Section 80C?

NRI cannot save tax under the Income Tax Act through Section 80C of the Income Tax Act. Instead, this facility is only provided to the resident Indians and HUFs.

Q.5 Whether an individual can claim relief under both employee and employer's contribution to EPF?

Employee and employer's contributions to EPF. The Income Tax Act allows only the employee's contributions as a deduction. However, the aggregate relief claimed should not exceed the overall limit of Rs. 1.5 lakh.

Q.6 Whether tuition fees paid on behalf of more than one child are eligible for deduction under Section 80C?

Under the Income Tax Act, an individual can claim deductions for the tuition fees paid for the education of two children. This includes all the fees paid to schools, colleges, universities, and other educational institutions in India.

Q.7 Whether donation is eligible for tax exemptions under Section 80C?

Section 80C of the Income Tax Act allows for tax exemption on contributions made to some funds and institutions.

Q.8 If a person borrows money for repair/renovation of a house, is it eligible for 80C?

A regular home loan is covered under 80C, but the loan taken for repairing and renovating the house is not.

Q.9 In case of provident funds, can the investment be made under EPF and PPF simultaneously?

If a person invests in both EPF and PPF, then he can claim both the investments under 80C of the Income Tax Act.

Q.10 Is the total amount of Rs. 1.5 lakh benefit under Section 80C available on a single investment?

No, the overall Rs. 1.5 lakh limit is applicable to all eligible investments and expenses under Section 80C. A combination of investments and expenses can be used to achieve benefits to the best extent.